The shipping rivals plotting divergent courses on global trade

Mediterranean Shipping Company and AP Møller-Maersk were always unlikely bedfellows. Yet in 2015, the world’s two biggest container shipping companies set aside their rivalry and shrugged off opposition from regulators to form a capacity-sharing alliance.

Maersk containers could be carried on MSC vessels and vice versa, cutting both groups’ operating costs without reducing the number of ports they could serve. The pact helped reshape container shipping, an industry whose profits had traditionally been tied to the ebbs and flows of the global economy. Within two years, other big players such as France’s CMA CGM, China’s Cosco and German liner Hapag-Lloyd had struck similar deals.

But now MSC, based in Switzerland but controlled by an Italian family, and Maersk, the venerable Danish conglomerate, are divorcing. This year they confirmed that the so-called 2M alliance will end in 2025. Eight years after the agreement began, the dynamics of the container shipping business are starting to change dramatically — in ways that have important implications for the future pattern of globalisation.

The context is the boom the two companies enjoyed during the Covid-19 pandemic. After years of highly cyclical and often weak earnings, shipping lines enjoyed record profits as ships queued up at ports to unload and customers raced to get goods on to a diminishing number of available vessels.

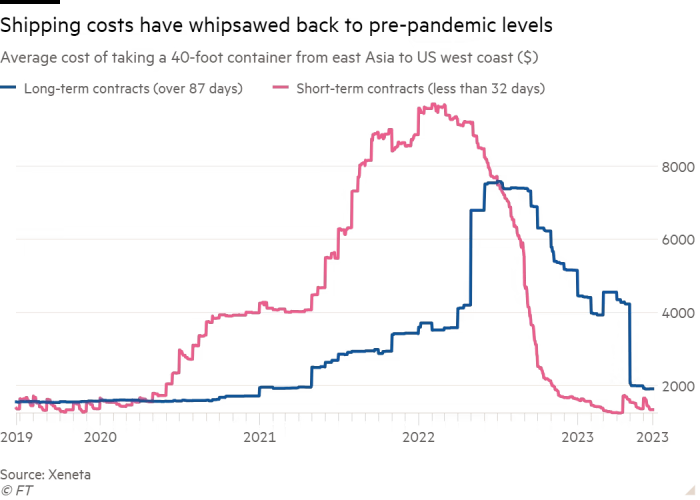

The average cost of shipping a 40ft container from eastern China to the US west coast at short notice rose from less than $2,000 to a peak of $9,699, according to data provider Xeneta. In the three years from 2020 to 2022, the industry generated as much profit as it had during the previous six decades combined, according to the shipping consultancy Drewry. Maersk’s annual pre-tax income soared from $967mn in 2019 to $30.2bn in 2022 — more than investment bank Goldman Sachs or Facebook-owner Meta.

“[Shipping lines] went into the pandemic barely breaking even,” says John McCown, founder of the shipping consultancy Blue Alpha Capital. But after Covid-19 hit and they immediately took vessels off the water and helped create the strongest “supply and demand dynamic ever”.

Bumper profits have given Maersk and MSC the freedom to sever ties and to invest heavily, but the two companies are taking strikingly different approaches to the future of their industry.

MSC has ordered a significant number of new ships and last year overtook Maersk in terms of tonnage — an apparent bet on the continued growth in global trade. Maersk, on the other hand, is investing in broader logistics facilities, such as new warehouses, trucks and planes, in an effort to appeal to customers worried about future supply chain disruptions.

About 90 per cent of global trade is transported by sea and between them, MSC and Maersk control as much as a third of the international container business. As trade disruptions during the pandemic showed, the decisions these companies make can have an outsized impact on international supply chains and the global economy.

As the two lines plot their very different courses, industry observers are uncertain which, if either, strategy will pay off. Large box carriers have more money “than they can use”, says Lars Jensen, chief executive of the shipping consultancy Vespucci Maritime. With trade now slowing after the dislocations of the pandemic, they have a rare opportunity to make that cash count.

Container ships anchored off the Californian coast wait to offload in 2021. Trade disruptions during the pandemic showed how shipping companies can have an outsized impact on the global economy © Mario Tama/Getty Images

But the years of abnormal profits have also drawn regulatory and public scrutiny, while owners of heavily polluting ships are under pressure to invest in curbing emissions. The industry that helped oil the wheels of globalisation must now weather its aftermath: reshoring and increased economic nationalism.

“The dice have been rolled,” says one shipping executive on MSC and Maersk’s diverging strategies. “It’s going to be a more exciting time to be in this industry.”

A long rivalry

Geneva, in landlocked Switzerland, is an unlikely location for the headquarters of the world’s leading container shipping group. But from its low-tax base, the former ferry captain Gianluigi Aponte has quietly built the MSC empire from a single cargo ship in 1970 to a worldwide fleet of more than 700 owned and leased vessels.Along the way, his family-owned business has acquired a reputation for being aggressive and nimble. As chair and president respectively, the secretive Italian and his son, Diego, retain tight control over the group, which does not disclose its profits and declined to put executives forward for interview.

Industry insiders described Maersk as a very different business, even before its recent expansion into warehousing. Founded in 1904, it has cultivated a reputation as one of the most reliable container shippers. Although the descendants of its founder, Arnold Peter Møller, still run its holding company, the shipper is now one of Denmark’s largest publicly traded groups, its quarterly earnings reports scrutinised globally as a barometer for international trade.

Their alliance was always a “marriage of convenience”, says Jensen. “You couldn’t find two carriers that were more different.”

People who have worked closely with both companies characterise the Danish group as a more unwieldy, bureaucratic machine than its competitor. “They are kind of opposites,” says a senior employee at one shipbroker. “Maersk is more corporate. MSC . . . has fewer people making more reactionary decisions. [When leasing a ship to MSC], we get a very quick reaction. Maersk decisions can take longer.”

That agility and the buoyant market conditions have enabled MSC to close the gap with its older rival, according to data compiled by the analysis firm MDS Transmodal. In 2019, Maersk was the market leader by capacity in 38 countries out of 153 served by container shipping lines, 10 more than MSC. But by the first quarter of this year, Maersk led in 30 countries, while MSC was the dominant carrier in 36, overtaking its rival in key markets such as the US and India.

“I have no doubt that MSC was more profitable than Maersk during these boom years,” says one person who knows the Aponte family well. “They maxed out and charged whatever they could for every container.” MSC declined to comment on its profitability but says it “invests in assets, equipment and people to continue to provide a good service to clients and play an essential role as a facilitator of global trade”.

The rivalry also took on a personal twist. In November 2019, Maersk abruptly announced the departure of its chief operating officer, Soren Toft, who had been tipped by some for the top job in the future. Instead, he joined MSC’s container shipping business as chief executive a year later, the first person from outside the Aponte family to take on a leadership role.

Toft has been “a great catch” for MSC, says the shipbroker’s employee. “He has all that experience from Maersk. [Maybe MSC] wanted to know what is going on inside Maersk. Maybe they needed that.”

Maersk’s chief executive, Vincent Clerc, stresses that his company can also flourish outside the alliance. The group “needed to regain control”, he says during an interview at its Copenhagen headquarters.

“It was just very difficult for us to do what we think is right [while] having to share so much,” he says, adding that Maersk and MSC had “very different views” on “cost versus quality trade-offs”.

“This is not about: only one strategy can win . . . we’re going in a certain way. We think that there is a market of customers for whom what we do makes it right to ship with us.”

Setting new courses

This is not the first time that Maersk has attempted to tilt its business beyond sea freight. Jensen, a former Maersk researcher, points out that the group tried to break into logistics about two decades ago, before the financial crisis of 2008 scuppered investment plans across the industry.Now, Clerc has set an ambitious target for logistics earnings to overtake those of the shipping operation within a decade. Its logistics and supply chain services unit generated a fifth of the group’s overall sales and less than 5 per cent of profits in 2022.

Vincent Clerc, chief executive of Maersk. His strategy for an expansion into logistics is pinned on the idea that it will make the company more resilient during economic downturns © Liselotte Sabroe/Ritzau Scanpix/AFP via Getty Images

Since 2019, the group has used its bumper earnings to acquire at least 11 companies, among them the $3.6bn takeover of LF Logistics last year. The Hong Kong group’s 198 warehouses helped Maersk double the number of sheds it owned that year.

Clerc’s hope is that a premium, end-to-end supply chain service will appeal to the big retailers whom it has focused on building relationships with. “In the Covid years, [supply chain] vulnerability was really laid bare,” he says. “The idea was [that] you create solutions for these large customers that, today, have to contend with very, very volatile supply chains.”

Maersk had been allocating more shipping capacity to customers most likely to buy into these solutions, and Clerc argues that Maersk’s expansion into logistics will make it more resilient during economic downturns.

But he risks antagonising the freight forwarders who handle cargo for smaller retailers and group it together to help fill containers. Its move inland is turning these businesses from customers into competitors. Jensen says that “quite a few” have told him over the past year that they are reducing business with Maersk because of its new strategy and a perception that the carrier has not recently offered them sufficient capacity.

The challenge for Maersk is growing its logistics business at scale, he says, since freight forwarders control as much as half of the world’s container cargo.

If MSC can grow its fleet fast enough, it could offer a cheaper alternative to these disgruntled customers. But along with other shipping groups who have invested heavily in new vessels, MSC is running the age-old risk: overcapacity.

Prior to the pandemic, shipping lines suffered “10 years of piss-poor markets”, says Niels Rasmussen, chief shipping analyst at the industry group Bimco. “But that to a certain extent was self-inflicted. Because just like now, they had ordered a lot of ships” during an economic boom. That meant the supply of shipping capacity significantly outstripped demand when global trade took a turn for the worse.

The Swiss group is awaiting the delivery of 122 ships, while Maersk has ordered just 28, according to the data provider Alphaliner. Driven in large part by MSC’s bulging order book, Bimco expects the total supply of container space across the industry to increase 12 per cent in the two years to 2024 — up to double the anticipated growth in demand.

The person close to the Apontes says the family still calls the shots at the Swiss-based group. “MSC has made a big bet on ordering new vessels and that is all [Gianluigi] . . . [He] has had this urge, this quest inside him to overtake Maersk. And he has pursued it year after year.”

As MSC and its peers wait for more vessels to roll down the slipways, profits have already nosedived. During Covid lockdowns, a boom in spending on gadgets, home gyms and hot tubs helped drive up the cost of shipping. Now demand has moderated, freight rates have crashed back down. Maersk forecasts its underlying earnings will fall by as much as 94 per cent this year.

Rasmussen expects box carriers will scrap older vessels at a faster rate in the years ahead, partly offsetting the new supply. He adds that they are already taking steps to limit supply, including skipping port stops and reducing vessel speeds.

Challenges ahoy

Even if the industry can mitigate its boom-to-bust tendencies, it faces the prospect of a stricter regulatory regime in the years ahead.This month, a judge at the US Federal Maritime Commission ordered a Maersk subsidiary to pay a Florida-based furniture importer $9.8mn in damages for lost profits and unlawful retaliation, after the firm alleged Maersk had withheld capacity and then unilaterally cancelled its contract, leaving it exposed to soaring spot rates. The same judge also made a $1mn ruling against MSC, which is set to appeal.

Soren Toft, chief executive of MSC’s container shipping business. Before his departure from Maersk in 2019, he had been tipped as a future contender for the top job © Oliver O’Hanlon/MSC

The widely reported cases have drawn attention to what some say is the excessive market power wielded by a handful of large shipping groups, whose decision to take scores of vessels out of action immediately after the Covid outbreak contributed to the capacity shortages and elevated freight rates in the ensuing months.

In 2022, President Joe Biden promised to “crack down on ocean carriers whose price hikes have hurt American families”, calling out the “nine foreign-owned carriers” who control most of the market. In June that year, Congress passed legislation that increased the FMC’s powers to stop these groups refusing or overcharging for cargo. Scrutiny has also intensified in France, where lawmakers called last year for a 25 per cent tax on the “superprofits” accumulated by Marseille-based CMA CGM, the world’s third-biggest carrier.

Clerc pushes back at suggestions that shipping groups have become too powerful, arguing “every shipping container was used” during the pandemic.

“I do understand the frustration. But this is similar to saying [during recent energy shortages] that these energy companies have too much power. If you have a limited supply of something, not everybody can get it.”

MSC said it had “invested considerably” and “deployed all available shipping capacity” to meet unprecedented surges in demand, softening the impact of lockdowns for consumers globally.

The industry is also bracing itself for new laws under which it will pay more for the greenhouse gas emissions from so-called “bunker fuel”, the heavy diesel oil used to power large ships.

The UN’s International Maritime Organisation previously mandated a target for shipping to halve annual greenhouse gas emissions between 2008 and 2050, short of the net zero ambitions set for other industries. But it has committed to strengthening that goal next month and, more recently, French officials have been rallying support for a global tax on the industry’s greenhouse gas emissions.

Maersk has ordered up to 19 green methanol-powered ships as it targets net zero emissions by 2040. But these are “dual-fuel” vessels, reflecting concerns that they may still rely on fossil fuels if the limited supplies of sustainable alternatives are not expanded in time.

For all these accumulating pressures, the industry’s closest watchers say that MSC and Maersk’s hold on the global supply chain is unlikely to loosen soon, even as they chart divergent courses.

“[Customers] are aware that carriers have more strength than they had in the past,” says McCown, of Blue Alpha Capital. “What came away from [the pandemic] is a renewed awareness among carriers that they can command their own destiny.”

Copyright : Financial Times